Restaurant operators, are you afraid of ghost kitchens? If not, should you be? You might even be wondering what a “ghost kitchen” is.

What is a Ghost Kitchen?

Ghost kitchen is the term used to describe a stand-alone commercial kitchen that doesn’t have a customer-facing dining room connected to it. Ghost kitchens are not a new development as restaurants have used them for some time to prep and precook offsite.

So there’s no need to be concerned about the growth in ghost kitchens alone. What should have you concerned is the restaurant marketplaces (see below) using ghost kitchens (instead of restaurants) to fulfill their orders. This combination has the potential to disrupt the restaurant industry, taking a significant portion of the revenue away from brick and mortar restaurants and giving the restaurant marketplaces a price advantage the customers can’t/won’t ignore.

Before we discuss how the restaurant operators should respond, let’s take a look at the two trends that are enabling this disruption of the restaurant market:

Food Delivery Growth

Pizza restaurant chains have been delivering for decades, originally via phone orders and increasingly over the past decade via mobile and online ordering. There isn’t much you can’t do with mobile phones these days and the Millennials are embracing them in a big way. Just look around and see how many people are looking a their phones, whether they’re sitting, walking, or (unfortunately) driving. People practically live through their phones these days. So it’s no surprise that mobile and online ordering for food delivery is a rapidly growing trend.

The food delivery growth projection everyone is quoting these days is from an 82-page report from the investment bank UBS titled “Is the Kitchen Dead?” which forecasts that delivery sales could rise an annual average of 20% from $35 billion to $365 billion worldwide by 2030. If this is even half correct, restaurant operators must have a solid delivery strategy to capture some of this growth.

Restaurant Marketplaces

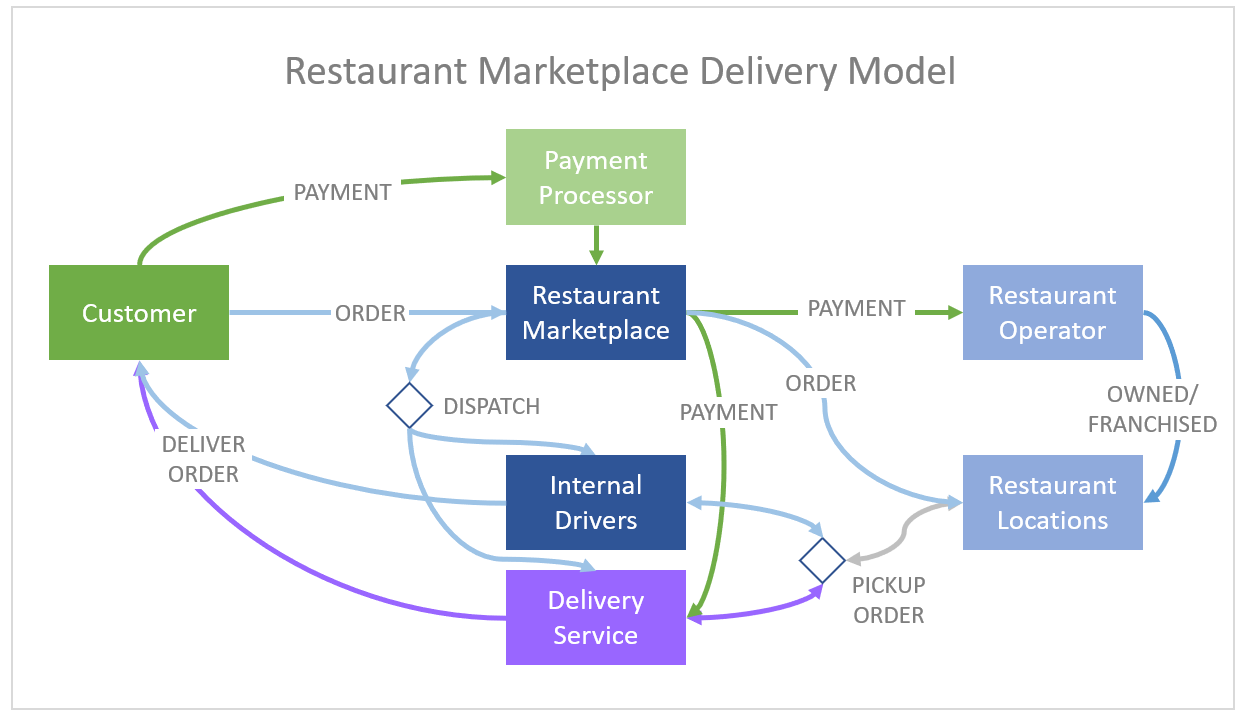

The next trend is the rise of the restaurant marketplaces, online marketplaces of restaurants where consumers can select a restaurant, place an order, and have the marketplace facilitate payment, fulfillment, and delivery of that order. Here’s a diagram of the restaurant marketplace delivery model:

The restaurant marketplaces are growing rapidly and there are several well-funded players competing for these mobile/web savvy consumer’s business. Here are just a few of the leading restaurant marketplaces today:

- GrubHub: an online marketplace with over 105,000 takeout restaurants in over 2,000 US cities and London. They reported over $5B in sales in 2018 (2018-Q4 40% YOY-quarterly growth, 2018 21% YOY-annual growth), processing 467,500 daily orders to 17.7 million active diners (source).

- UberEats: Uber, a ride-share marketplace with 3 million drivers, entered the restaurant marketplace business 3 years ago to leverage their driver network to deliver food orders.

- Amazon Restaurants: Amazon debuted in Seattle in 2015 and has expanded to 20 US cities and London.

- EatStreet: an online marketplace with 15,000 takeout restaurants in over 250 cities and 1.7 million active users (as of 11/8/17, source).

- Just Eat: London-based online marketplace with over 100,000 takeout restaurants (across the UK, Australia, New Zealand, Canada, Denmark, France, Ireland, Italy, Mexico, Norway, Spain, Switzerland, and Brazil) and 26 million customers (source).

- Deliveroo: London-based online marketplace launched in 2013 with 20,000 takeout restaurants in the UK (source).

Given the growth of these restaurant marketplaces, the restaurant operators can’t ignore them and can’t realistically turn their orders away. This restaurant marketplace delivery model also creates many challenges for the restaurant operators:

- Profits: my clients tell me the restaurant marketplaces are taking 20-30% commissions plus adding a delivery fee to their orders. This means the restaurants are breaking even or losing money on each of these orders. The argument for this arrangement is that it could be a new customer that will go to a competitor if you don’t accept the order. So restaurant operators do their best to entice these customers to join their loyalty programs and use their mobile app or website for future delivery orders. Since they’re not delivering these orders, restaurant operators can only advertise their loyalty program and direct mobile/online ordering options on the food packaging.

- Reconciliation: you may have heard of the term “wall of tablets” in the restaurant business. Since many restaurant marketplaces aren’t integrated with the restaurant’s Point of Sale (POS), the restaurant is forced to receive orders via a tablet and manually enter the orders into their POS. This manual entry presents a reconciliation nightmare for restaurant operators to match up these orders with the quarterly payments received by the restaurant marketplaces.

- Data: data is everything in the new connected economy. Online retailers have been leveraging customer data for decades to customize and optimize how they market to each individual customer as well as inform marketing and product decisions. Restaurant operators are playing catch-up in building out these capabilities. To make matters worse, restaurant operators have no customer data when an order comes from a restaurant marketplace. This gives the restaurant marketplaces a huge advantage over the restaurant operators.

- Execution: since the order marketplaces are still working to integrate with the vast number of POS solutions used by the restaurants, orders are still manually entered in many cases. This is a recipe for failure if the order isn’t entered into the POS immediately or if it is keyed in incorrectly. There’s also a big challenge in making sure the menus on the restaurant marketplaces are accurate and able to be fulfilled by a given restaurant location. This is why the restaurant marketplaces are acquiring the mobile/online order engine technology vendors (ex: Uber acquired Ordertalk and GrubHub acquired Takeouttech and LevelUP).

- Quality: as mentioned in the previous bullet, manual entry opens up the possibility that the order is incorrectly fulfilled. Another potential quality issue is that the restaurant marketplaces don’t have the same ordering rules that the restaurant operators build into their POS platforms. An simple example is an item selected prompting required modifiers to be selected.

- Experience: restaurant operators give up control of the customer experience when a restaurant marketplace handles the ordering and delivery process. If there are execution or quality issues, the customer often applies some or all of the blame to the restaurant operator.

As you can see, this model is no picnic for restaurant operators. They would gladly turn the restaurant marketplace orders away if that didn’t mean directing business to their competitors.

Will Marketplaces Disrupt Restaurants?

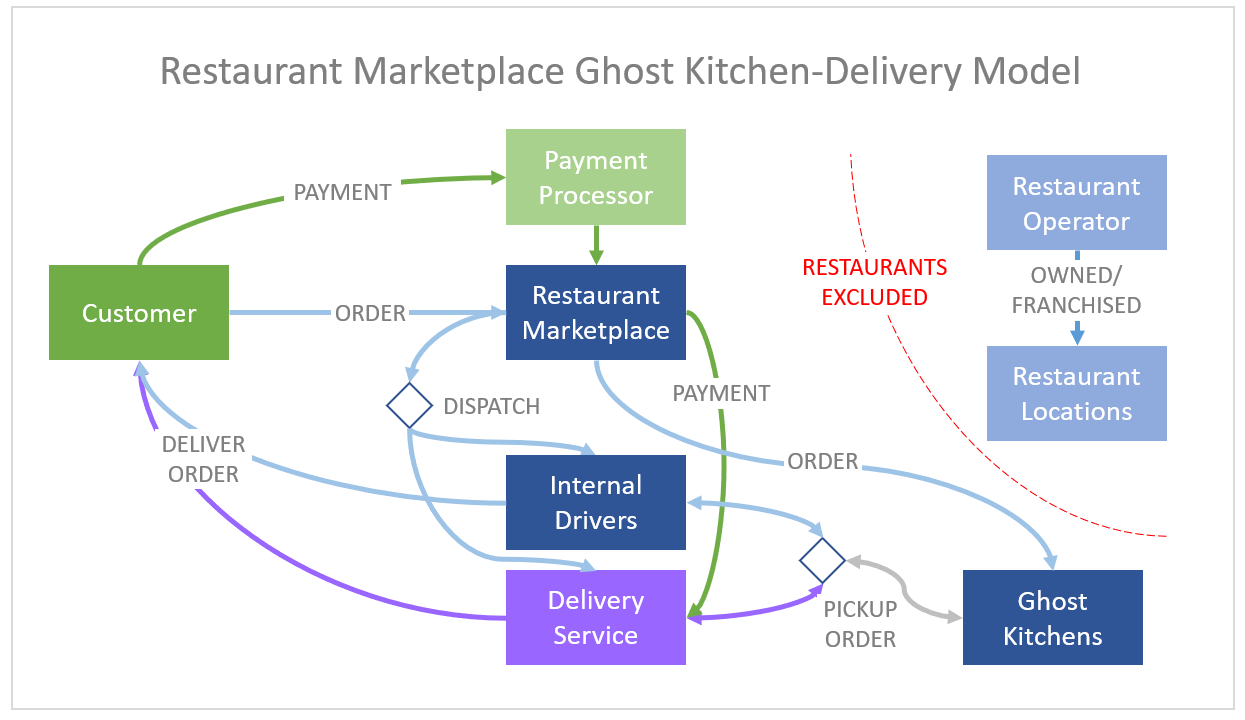

Now that we’ve established the delivery and restaurant marketplace growth trends and the challenges this model brings to the restaurant operators, let’s return to the question of this article. Should restaurant operators be afraid of ghost kitchens? The answer is no. What they should be afraid of is the restaurant marketplaces using their own ghost kitchens and delivery to cut the restaurant operators entirely out of the picture.

In the diagram above, the dark blue boxes represent the restaurant marketplace-owned functions. By using their own ghost kitchens to fulfill orders, you can see how the restaurant operators are excluded from the model.

Here are a few advantages the restaurant marketplaces have that will enable them to disrupt the restaurant business with this model:

- Data: while a restaurant operator has data about what a specific customer orders from them, they don’t have visibility to what that customer orders elsewhere. On the other hand, the restaurant marketplaces do have this information. This will enable them to mine the data to tell them what the most profitable menu of items are for a specific geographic area. For example, they may know that 300 customers in a specific town order an average of 3 all-meat pizzas each month. They can then do two things with this information: 1) market a lower cost option specifically to those 300 customers, and 2) procure ingredients for those 900 pizzas/month to that town’s ghost kitchen. By predicting based on buying patterns, they can minimize waste and over-supplying inventory in a kitchen.

- Pricing: costs are lower for ghost kitchens because they can be located in less-expensive real-state and don’t require the parking, dining room, or staff to serve the customers. This gives the marketplace-ghost kitchen-delivery model a significant price advantage.

- Profits: add the lower costs to customers being conditioned to paying more for a delivery order and you have a recipe for higher profits.

These advantages should cause the restaurant operators to take notice. But there is still a way for restaurant operators to win this ghost kitchen-delivery model over the restaurant marketplaces. To do this, they must disrupt themselves before the restaurant marketplaces disrupt them. A great example of disrupting yourself is Netflix creating the video streaming business that eventually disrupted their video-mailing business. Restaurant operators can do the same.

How Restaurants Can Disrupt Themselves

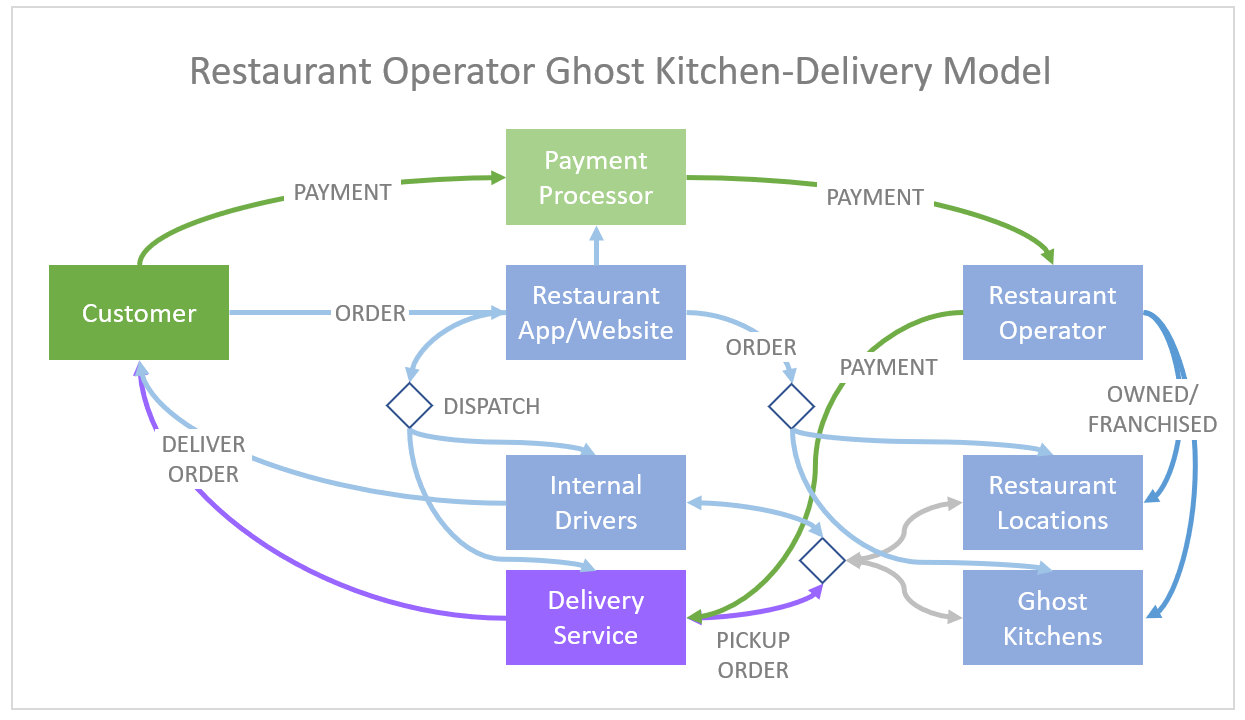

How can a restaurant operator disrupt their existing business? By implementing their own ghost kitchen-delivery model. Here’s an illustration of this model:

Restaurant operators pursing this model will need to embrace an omni-channel business model with ghost kitchen-delivery being a new channel. The strat-plan for this channel will need a comprehensive game plan that addresses technology, ghost kitchens, and delivery:

- Technology: build the optimal guest experience for your brand with mobile/online ordering technologies. Grow this channel with customer acquisition, loyalty, management, and analytics technologies. Execute by leveraging kitchen and delivery management technologies.

- Ghost Kitchens: experiment with your own kitchens, leverage existing multi-tenant kitchen centers (ex: Kitchen United, Cloud Kitchens), or both. Consider exploring dark kitchen concepts in the future by leveraging automation/robotics to prepare or assist in preparing food, lowering the cost of labor.

- Delivery: build delivery capability using your own drivers, delivery service providers (ex: DoorDash, Postmates, Caviar, Favor, DeliverLogic), or both. As an example, Chipotle reports a 667% increase in weekly delivery orders since initiating a partnership with DoorDash. Consider exploring drone delivery in the future (sound far fetched, take a look at this April Fools video).

This game plan should also consider how to address some of the risks/challenges inherent with this channel. For example, this channel will likely cannibalize current brick and mortar economics (especially an issue with franchisee locations). This channel may require a new business unit to ensure this channel’s priorities don’t get squashed by brick and mortar restaurant channel’s needs. Leveraging existing restaurant location kitchens for delivery may create capacity issues in those locations and require re-configuring the take-out pick-up area for higher volumes. Leveraging a third-party delivery service may have similar customer experience/services challenges experienced in the marketplace delivery model. Lastly, current menus may need to be modified to ensure food quality when delivered by using different packaging and cooking temperatures.

Regardless of these challenges, the restaurant operators can still prevail and win with the ghost kitchen-delivery model.

Previously, we outlined the advantages the restaurant marketplaces have over the restaurant operators. Here are some of the advantages the restaurant operators have in pursuing the ghost kitchen-delivery model:

- Brand Awareness: already have an existing loyal base of clients to market to and convert to the delivery model.

- Brand Trust: already have customer’s trust in their product quality, something the restaurant marketplaces will need to build if they begin selling their own products.

- Infrastructure: already have an existing infrastructure of kitchens, cooks, and sourcing/distribution networks in place.

- Time: able to deploy quickly by leveraging existing restaurant kitchens and a third-party delivery service provider.

If the ghost kitchen-delivery model does end up disrupting the restaurant industry (regardless of which model above wins), restaurant operators will need to focus on creating a premium customer experience that can’t be achieved by customers through home delivery. Think of how the movie theaters have had to create a premium customer experience now that home theater technology has become so affordable.

Restaurant operators should consider creating a premium restaurant dining experience as well, while at the same time embracing a ghost kitchen-delivery model to give their customers both options. If a customer loves your brand and your product, let them decide whether to be served with a premium experience at your restaurant or with a home delivery experience (and by leveraging the ghost kitchen-delivery model providing you with a more profitable order).

In closing, we caution restaurant operators not to wait too long to embrace the ghost kitchen-delivery model or the restaurant marketplaces will eventually catch up and the above advantages will disappear.